Principal Component Analysis (PCA) on Stock Returns in R

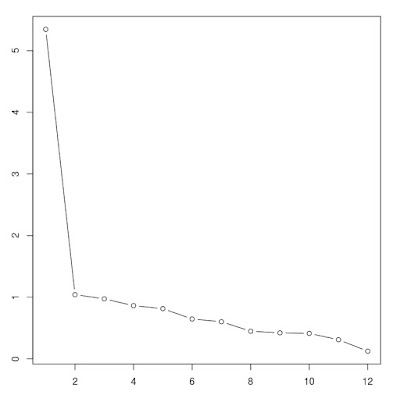

Principal Component Analysis Principal Component Analysis is a statistical process that distills measurement variation into vectors with greater ability to predict outcomes utilizing a process of scaling, covariance, and eigendecomposition. MS Azure Notebook The work for this is done in the following notebook, Principal Component Analysis (PCA) on Stock Returns in R , with detailed code, output, and charts. An outline of the notebook contents are below. Overview of Demonstration Supporting Material Pluralsight Explained Visually Wikipedia Load Data: Format Data & Sort Prep Data: Create Returns Generate Principal Components Eigen Decomposition and Scree Plot Create Principal Components Analysis FVX using PCA versus Logistic Regression Alternative Libraries: Psych for the Social Sciences